Which is Best For Taking A Policy Annuity or Life Insurance

Best For Taking A Policy Annuities or life insurance

Table of Contents

Whenever you want to be sure that your family will be taken care of financially in the years to come, you should think about purchasing a life insurance policy or an annuity. On the other hand, you could still have some unanswered doubts regarding which alternative to go with and what the primary distinctions between the two are.

What exactly is an annuity?

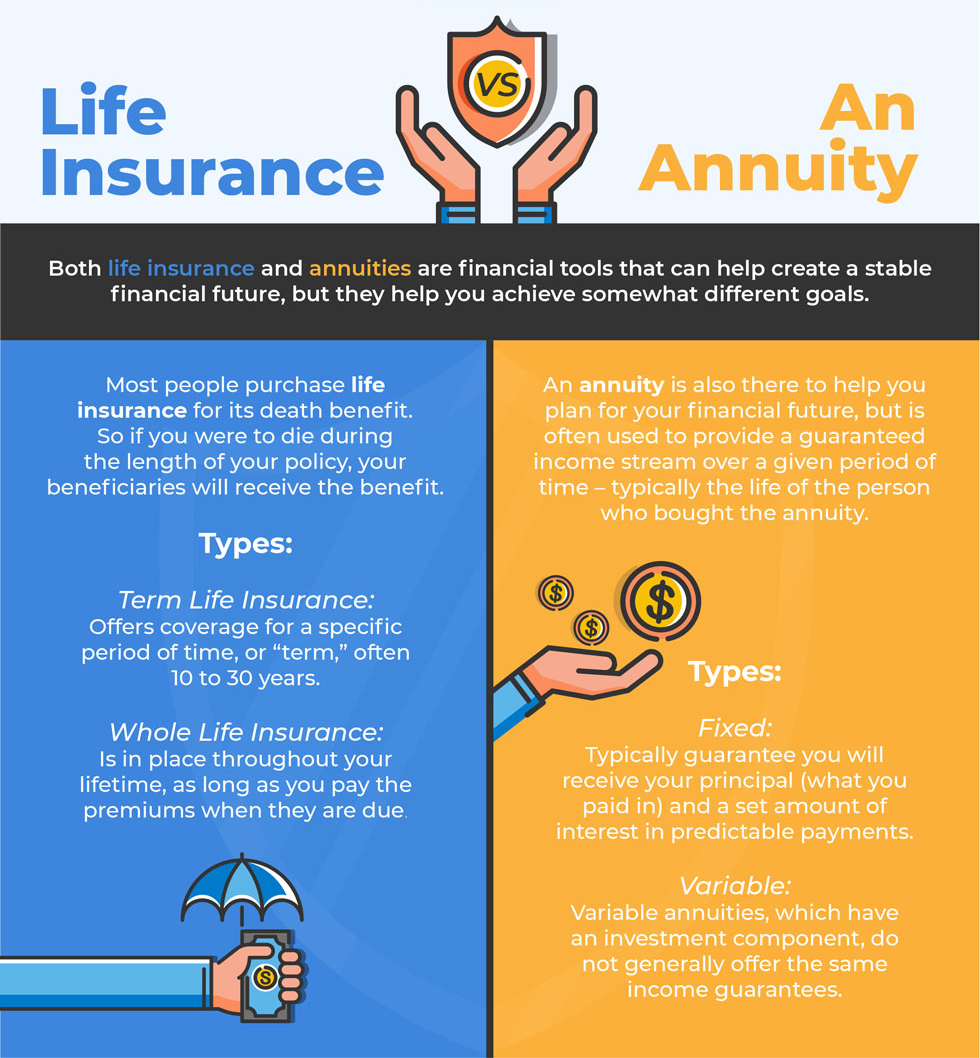

The owner of the policy and the insurance company enter into a certain kind of agreement known as an annuity. There are many variations of annuities, but the goal of each one is the same: to deliver a steady stream of income on a monthly basis for as long as the annuity holder lives. The price of the annuity is determined both by the kind of annuity and by the company that issues it. One of the drawbacks of annuity is that plans often come with a variety of fees, which may cause the overall cost to be greatly increased. They may also be difficult to get away of, and if you are interested in dissolving the annuity, you may be liable for a significant surrender charge. If you wish to get clear of them, you might also have to pay the cost.

Customers often invest in annuities due to the desire the peace of mind that comes with a guaranteed payment. Investing in the traditional stock market does not give any form of assurance, which might make customers feel as if they are taking on more risk. An annuity, as contrast to life insurance, is only obligated to provide payments so long as the individual who owns it is still living. Should you pass away, the annuity will come to an end. Customers who are concerned that they may outlive their retirement funds might acquire an annuity that comes with payments that are guaranteed for life.

What does it mean to have life insurance?

In the event that you die away while your life insurance policy is still in force, your beneficiaries will receive a death benefit from the policy. If there are individuals in your circle of relatives who are financially reliant on you after your death, purchasing life insurance might be the best way to ensure that they are able to do so. The majority of individuals only get life insurance when they possess a dependent spouse or kid who would suffer financially in their absence. You may be eligible for life insurance plans via your place of employment; however, you also have the option to obtain life insurance policies from independent insurance agencies.

Different kind of life insurance

The three most common kinds of life insurance are called term, whole life, and universal life. To choose the plan that is going to work out best for you as well as your family, it is essential to have a solid understanding of how the various plans operate.

Insurance on a term basis

In the case of term life insurance, coverage is provided for a certain amount of time, often ranging from ten to thirty years. During that time period, you are required to make contributions to the insurance organization on a monthly basis. Should you die away while the term is still active, the payoff in its whole will be given to your heirs. The total amount of the premiums you pay each month for a term life insurance policy is determined by a number of criteria, including your age, gender, and health. The more senior you are, the higher your rate will be.

Whole life insurance

The purpose of purchasing comprehensive life insurance is to ensure that you are protected during your whole life. In so far as you continue to pay the required monthly payments, the recipients will be qualified to receive a payout from the insurance policy. The rates for whole life insurance are much higher than those for term insurance due to the longer expected duration of coverage.

The majority of individuals don’t require insurance that will cover them for their whole lives, which is why many people who are specialists in finance believe whole life plans are unnecessary. When you retire, it’s possible that your family will no longer depend on what you make and won’t have a need for coverage in the event that you die away.

Universal Insurance

A universal existence policy, akin to life insurance for the entirety, will remain in effect for the whole of your life. On the other hand, universal life insurance might additionally arise with an amount of cash that can be used as a source of liquidity while the policyholder is still living. You may also utilize the amount of cash remaining to make the regular premium payments.

But, in most cases, this option will not be accessible to you until you have made installments on the policy for a number of years. The value of the money is placed in stocks, but the insurance provider places a cap on how much may be made from those investments. Universal life insurance plans have monthly rates that are comparable to those of whole life insurance policies.

How to Determine Which Is Right for You: Life Insurance or Annuities

You need to determine what you want from a financial product like life insurance or an annuity before you can make a decision between the two. Is it money that you have set up for your loved ones in the event that you die away when you are still in your prime working years? Is that a savings account that you plan to utilize when you reach retirement age? Finding out what motivates you is the first step in selecting the best suitable product for your needs. If you are interested in making financial preparations for retirement, it is possible that a 401(k) retirement savings plan or an Individual Retirement Account (IRA) could be a better choice for your needs than annuities or life insurance coverage.

It is not often recommended to put money into insurance policies or annuities as a kind of investing. It is nearly usually the case that contracts and life insurance policies have limitations placed on how much money you may earn in just one year. These caps can be detrimental to your savings. It is possible that short-term life insurance is the best choice for you when you want to safeguard the people you love financially in the event that you pass away. Term life policies have lower premiums than whole or universal policies, which means that you will have more money available for other purposes, such as saving. When it comes to making judgements of this kind, you should always seek the advice of an experienced financial expert.

Leave a Reply