Importance of CIBIL Score in Mortgage Loan and How to Improve CIBIL

CIBIL Score in Mortgage Loan

Table of Contents

CIBIL Score in Mortgage Loan which is why your CIBIL Rating is all about, will increase when you behave responsibly with your money and complete your financial obligations on time. Additionally, your credit worthiness will improve as a result of this improvement.Even before you think about making an application for a loan, you ought to verify your CIBIL rating, often known as your credit score. This piece of advice comes from everyone who has ever acquired a property using financing.

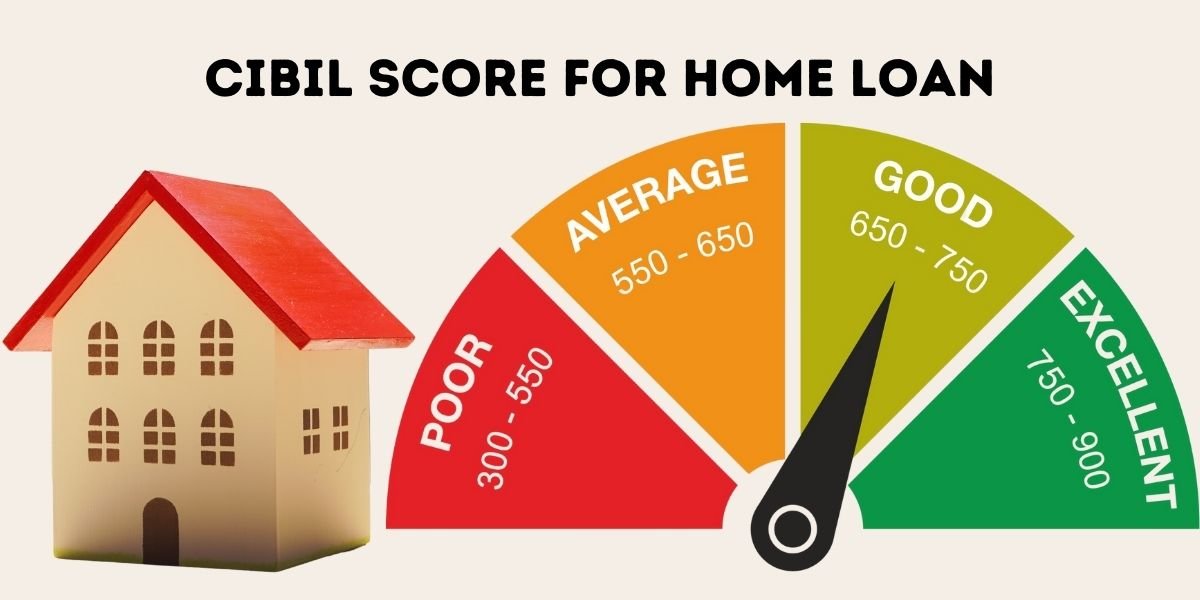

This crucial CIBIL Score is nothing more than a rating that the Credit Information Bureau (India) Ltd., often known as CIBIL, gives to the applicant for a loan based on how creditworthy they are. Individuals and business companies are both given a score by the Credit Bureau, which is another name often used for CIBIL. This score depends on data that the Credit Bureau obtains from financial institutions, such as bankers and other financiers, about the prospective borrower’s credit history, which includes repaying of loans and paying of credit card payments.

This article will offer you with an explanation of reasons the loan request was not sanctioned and how to guarantee that this does not happen again in the future if you already applied seeking a loan and it was not approved. It will offer you with direction about what we need to bear in mind to guarantee that you’re financially sound in the event that you are interested in applying for a house loan at some point in the future.

Why is The loan Applications rejected?

There may be several different scenarios that might lead to the denial of a loan application. The following are some general categories that may be used to classify these: Your payment history may be considered poor if you have a history of producing payments that are late or defaulting on EMIs. Both of these behaviours are indicators of potential financial difficulties and will adversely impact your CIBIL score.

Use of credit without moderation: Although a high utilisation rate will not directly damage your score, a rise in the amount you have remaining is a clear sign of an increasing payment load, and this might effect your score in a negative way. A greater proportion of unsecured loans—having a relatively large proportion of unsecured financing, such vehicle and/or personal financing, is going to have an adverse effect on your credit score. It is advisable to have a combination of secured (which belongs mortgages) and unsecured loans in one’s financial portfolio.

Opening of new numerous accounts – If you recently submitted applications for several credit cards and/or created accounts for personal loans, it is probably than the lending institution will look at your latest request with a certain amount of anxiety since you have recently established many accounts for either kind of financial product. The existence of many accounts is indicative of an increased debt load, which will undoubtedly have an effect on your score and may ultimately result in the rejection of your application.

Negligence while terminating an account – while closing an account, the account holder may sometimes fail to complete all the required formalities and processes or may leave a tiny amount outstanding as a result of an oversight. A negative influence is made on the credit score by this account’s existence, which continues to appear in the account holder’s outstanding obligations.

As a display of goodwill and friendship, we often sign our names as a guarantee for a person we know and consider to be a buddy or acquaintance. Any fail on the side of the borrower would have a negative influence on your score, therefore providing a guarantee ought to be a rational rather than an emotional choice for you to make. Negative statements on your credit record It goes with saying that comments such as “Written off” or “Settled” on your CIBIL report, in relation to earlier borrowings, give an unfavourable signal to lenders. This is because these phrases indicate that the debt was paid in full.

Why Should Anyone Increase their CIBIL Score?

It’s possible that increasing your CIBIL score won’t be all that challenging; all you have to do is make sure you’re paying attention to the things I’ve listed below. Pay-up is not making payments when you feel like it or when you have a good balance in your account, but rather making payments when they are due. Lenders look askance at borrowers who make their payments late, thus this behaviour should be avoided at all costs.

Low financial leverage is minimising the amount of money you borrow and the amount of credit you need. It is necessary to discourage the practise of applying for a loan. Ask yourself whether you truly need that loan or if the necessary cash can be obtained from other sources. whether it can, ask oneself if you really need the loan. Don’t get a loan until you really need the money.

Borrowings from a variety of sources – Ensure that you have a balanced portfolio of loans, including mortgage, personal, and vehicle financing. A slight lean towards obtaining a house loan (also known as a secured mortgage) could be useful. However, you should make sure that the scales are not extremely tipped in one direction. Keep it accurate – If there are errors in the records of your own bank account or credit card statements, immediately engage with the lender and make sure that they are fixed; otherwise, your credit rating will suffer through no fault of your own, as a result of a misunderstanding or an oversight. If there are errors, keep it accurate.

Do not permit defaults on shared account payments and do not guarantee a person who could default on their payments; doing any of these things might be just as bad to your CIBIL score as not making payments on any of your individual accounts.

Could your residence loans Increase your CIBIL Score?

Your CIBIL Score may increase if you take out a house loan, which might come as unexpected to you given the previous statement. Your CIBIL score will go up if you take out a secured loan, such as a mortgage, but it will go down if you take out an unsecured loan, such as a car loan or a personal loan, for example. The reasoning for this is rather straightforward: whilst secured loans are often used for the production of a growing asset, unsecured loans are typically used for the payment of an asset that is decreasing in value.

Therefore, if you are considering taking out a mortgage loan, it is essential that you select a financial institution that operates in an honest and open manner. If your application for a house loan is denied due to a poor CIBIL score, the lender need to acknowledge that it is their duty to inform you of this.

- cibil score and home loan interest rate

- cibil score for mortgage loan

- cibil score home loan

- CIBIL Score in Mortgage Loan

- credit score in loan mortgage

Leave a Reply