What Role Salary Play In Calculating Credit Score

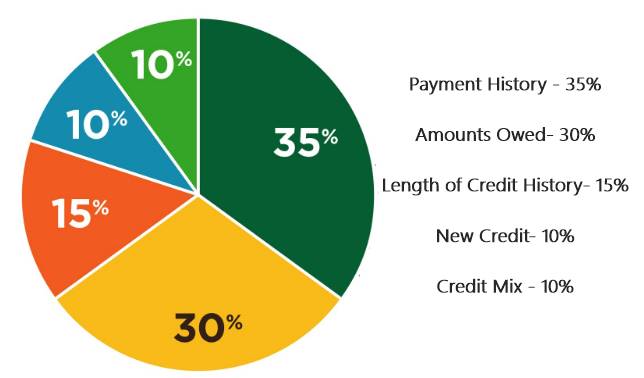

Salary Play In Calculating Credit Score Would you realise that your credit score does not take your salary into account? Although income does not have an immediate effect on your credit score, lenders may look at it if they think it may impair your capacity to make loan payments on time. The criteria that do determine your credit rating might […]